Fed vs. Geopolitics creates Markets Version of March Madness

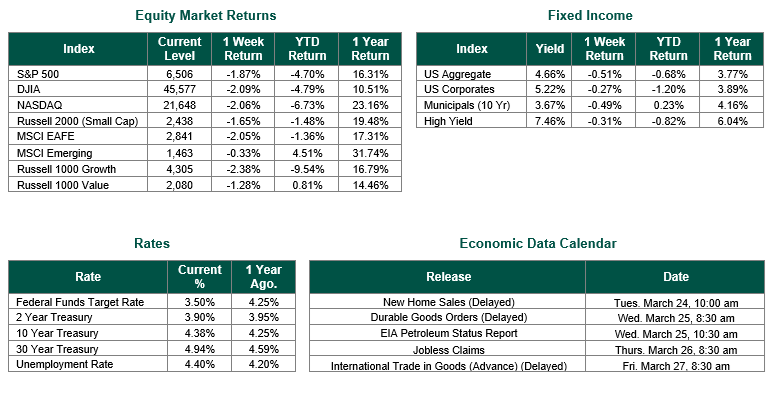

Global equity markets finished lower for the week. In the U.S., the S&P 500 Index closed the week at 6506, down 1.87%, while the Russell Midcap Index fell 2.18%. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -1.65% over the week. As developed international equity performance and emerging markets were lower, returning -2.05% and -0.33%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 4.38%.

Markets followed a now-familiar script last week: a promising start to the week quickly gave way to a late-week selloff, leaving stocks modestly lower for the fourth consecutive week. The S&P 500 closed Friday down roughly 1.5% on the day and now sits approximately 5% below its January all-time high. Small caps entered correction territory, defined as a 10% decline from a recent peak, while the Dow closed below its 200-day moving average for the first time since mid-2025. Energy was the lone bright spot for a second consecutive week, buoyed by elevated oil prices. Technology and financials also held modest gains, while utilities, real estate, and consumer discretionary bore the brunt of the week’s declines.

The U.S.-Iran conflict remained the dominant force driving markets. Israel struck Iran’s South Pars gas field, the world’s largest natural gas reserve, and Iran responded by targeting energy infrastructure across the region, rattling global commodity markets. Oil prices remained stuck near $100 per barrel, with Brent crude settling above $108 at points during the week. A brief moment of optimism emerged Thursday when Israeli Prime Minister Netanyahu suggested the conflict could end sooner than expected, sparking a late-session rally that lifted stocks off their lows. Still, the situation remained unresolved heading into the weekend.

The Federal Reserve held rates steady at its March 18-19 meeting, keeping the federal funds rate in the 3.50-3.75% range. The decision was widely expected, but the meeting’s tone was notably more hawkish than in prior gatherings. The Fed raised its 2026 inflation forecast to 2.7%, up from 2.4% in December, citing upward pressure from tariffs and elevated oil prices. Chair Powell acknowledged that a rate hike was discussed at the meeting, though he noted it is not the base case. The Fed’s “Dot Plot” chart still shows one cut in 2026, but futures markets have moved well past that projection — pricing in no cuts this year, with the next reduction not expected until mid-2027. The narrative has shifted meaningfully: earlier this year, markets were debating when the Fed would cut; now the question is whether it will cut at all this year.

Economic data offered little comfort last week as weekly jobless claims, while declining modestly, reflected a labor market in a holding pattern of low hiring and low firing. The Treasury curve flattened on the week, a signal that bond markets are pricing in a prolonged period of elevated short-term rates. Inflation expectations in the short- to medium-term continued to drift higher, driven by energy prices and tariff uncertainty, though longer-term inflation expectations remained relatively anchored.

The trajectory of the Iran conflict remains the single biggest variable for markets heading into the new week. Any credible sign of a ceasefire or diplomatic off-ramp could provide meaningful relief to both oil prices and equity sentiment. This possibility was certainly the case as we start this new week, as President Trump indicated that the U.S. and Iran had had productive conversations regarding a resolution of hostilities in the Middle East and that the U.S. has postponed any potential strikes against Iranian power plants and energy infrastructure for a five-day period. Oil prices fell, and stock prices soared following this announcement. Of course, time will tell whether hostilities further de-escalate or re-escalate during and after the next five-day period.

Best wishes for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 3/20/26. Jobless claims sources from the Bureau of Labor Statistics on 3/19/26. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate risk and volatility in your portfolio, but it does not guarantee profits or protect against losses.