Economic Data Momentum Not Good Enough for Markets

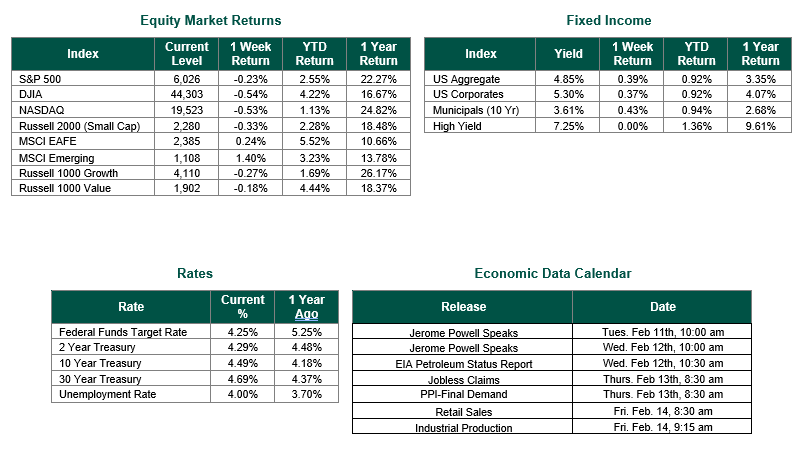

Global equity markets finished mixed for the week. In the U.S., the S&P 500 Index closed the week at a level of 6,026, representing a decline of -0.23%, while the Russell Midcap Index moved – 0.51% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -0.33% over the week. Developed international equity performance and emerging markets were positive, returning 0.24% and 1.40%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 4.49%.

As we mentioned last week The U.S. economy continues to demonstrate resilience despite prevailing uncertainties. Q4 2024 GDP growth reached 2.3%, contributing to a full-year growth rate of 2.8%. Early 2025 indicators suggest ongoing strength, with Q1 GDP projected to exceed trend levels at 2.9%. Consumer spending, representing 68% of GDP, remains robust, growing at a healthy 4.2% in Q4 2024. Adding to the positive momentum from the week prior, the manufacturing sector is showing signs of recovery, with the U.S. manufacturing PMI recently signaling expansion for the first time since 2022.

The Q4 2024 earnings season is also exceeding expectations, with 77% of reporting S&P 500 companies surpassing forecasts according to FactSet. Looking forward, corporate tax policy and deregulation will be key areas of focus. Favorable policy updates in these areas could further enhance market sentiment.

Finally, the January jobs report underscores the labor market’s continued strength. While total jobs added fell slightly short of expectations, upward revisions to prior months resulted in a healthy three-month average of 241,000. The unemployment rate declined to 4.0%, significantly below the long-term average. Wage growth ticked up to 4.1% year-over-year, potentially putting upward pressure on inflation but also supporting consumption through positive real wage gains. While mindful of potential headwinds, current economic, earnings, and labor market data paint a positive picture for the near term.

Best wishes for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 2/7/25. Earnings data from FactSet on 2/7/2025. Employment data sourced from the Bureau of Labor Statistics on 2/7/2025. Economic Calendar Data from Econoday as of 2/10/25. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.