Economic Fears Push Nasdaq into Correction Territory

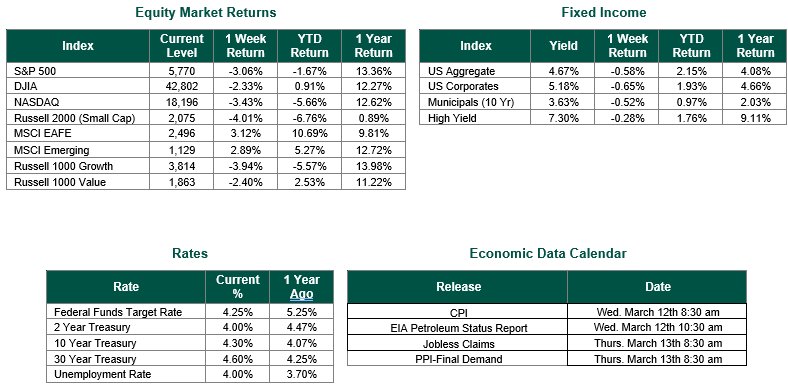

Global equity markets finished mixed for the week. In the U.S., the S&P 500 Index closed the week at a level of 5,770, representing a decline of -3.06%, while the Russell Midcap Index moved down -3.50% last week. Meanwhile, the Russell 2000 Index, a measure of the nation’s smallest publicly traded firms, returned -3.05% over the week. Developed international equity performance, as measured by the MSCI EAFE Index, was up 3.12%, while emerging markets, represented by the MSCI Emerging Markets Index, increased 2.89%. Finally, the 10-year U.S. Treasury yield moved up, closing the week at 4.30%.

Last week, the U.S. stock market experienced significant volatility, with the S&P 500 Index posting its worst weekly decline since September 2024. The decline resulted from a turbulent period driven by uncertainty over President Trump’s tariff policies, including a 25% levy on imports from Canada and Mexico, which he later partially rolled back.

The tech-laden Nasdaq entered correction territory, down over 10% from its recent highs, over fears that slower economic growth may ultimately result in a recession. While a recession is not our base case in 2025, an economic slowdown and a weakened jobs market do seem highly probable at this time.

Despite Friday’s rebound in stocks —the S&P 500 gained 0.5% after Federal Reserve Chair Jerome Powell called the economy “solid” — the week underscored broader economic concerns. Powell noted the Fed’s cautious stance on rate cuts, with a 91% chance of a pause in March, per the CME FedWatch tool.

Last week, we also learned that the U.S. added 151,000 jobs in February, below the expected 170,000, and the unemployment rate rose to 4.1%, signaling a cooling labor market. Manufacturing data earlier in the week also pointed to a slowdown, compounding tariff-related jitters.

Finally, oil prices hit their lowest level since 2021, while 10-year U.S. Treasury yields rose slightly to 4.31%. Overall, last week painted a picture of a fairly resilient yet rattled market navigating policy uncertainty and softening economic signals.

Best wishes for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 2/28/25. Jobs and Unemployment data from the Bureau of Labor Statistics on 3/7/25. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.