Fed Cut Rates but Turns More Hawkish

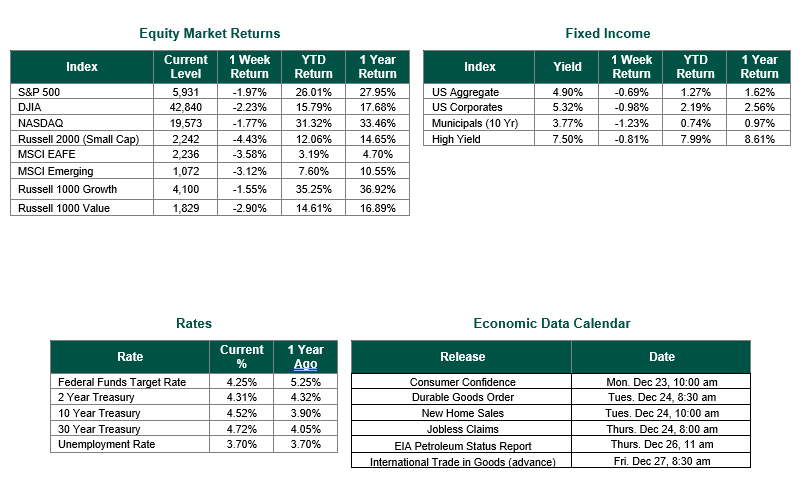

Global equity markets finished lower for the week. In the U.S., the S&P 500 Index closed the week at a level of 5931, representing a decrease of 1.97%, while the Russell Midcap Index moved -3.26% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -4.43% over the week. As developed international equity performance and emerging markets were lower, returning -3.58% and -3.12%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 4.52%.

As we near the end of the current year, investors are still digesting the results of the Federal Reserve’s meeting last week and determining how monetary policy will affect the economy in 2025. Below are some of our key outtakes from the Federal Reserve’s final FOMC meeting of 2024.

As widely expected, the Federal Reserve announced a rate cut of 25 Bp (0.25%) last Wednesday, which brings their total rate cuts this year to 100 Bp (i.e., 1%) and the Federal Funds Target Rate to a range of 4.25%-4.50% (the lowest range since December 2022).

Looking ahead, according to their updated Dot Plot chart, the Fed is now forecasting 50 Bp in additional rate cuts in 2025 (down from their 100 Bp forecast in September) and another 50 Bp in rate cuts in 2026 (in line with their forecast in September though landing at a higher year-end range as a result of the fewer cuts in 2025). These cuts align with their updated long-run neutral rate expectation for the Federal Funds Target Rate of around 3.0% (up from 2.9% in September).

As a reminder, there are eight FOMC meetings each year, with an updated Dot Plot Chart and Summary of Economic Projections published once per quarter following the meetings in March, June, September, and December.

The Fed is now also forecasting the following within the Summary of Economic Projections:

• Unemployment to end 2024 at 4.2% (was 4.4% in September) and increase slightly to 4.3% at the end of 2026 (in line with their September forecast)

• Inflation (as measured by Core PCE) to end 2024 at 2.8% (was 2.6% in September) and fall to 2.2% target by the end of 2026 (was 2.0% in September)

• Real GDP growth to end 2024 at 2.5% (was 2.0% in September) and slow to 2.0% through the end of 2026 (was also 2.0% in September)

We believe that the Fed will adopt a more gradual pace of easing in 2025 and 2026 with no single rate cuts of greater than 25 Bp until the Fed Funds Target Rate is closer to their new long-run neutral rate expectation of 3% (which may not be achieved by the end of 2026), given the many uncertainties surrounding the labor market, inflation, potential tariffs, and the policies to be implemented by the incoming administration.

In conclusion, according to the Fed’s forecasts above, rates, yields, and inflation should all be lower, and economic growth should be relatively stable over the next two + years. This longer-term outlook bodes well for both stocks and bonds, but the next two years will likely look very different than the last two years, and investors would be wise to plan and adjust their portfolios accordingly.

Best wishes for a wonderful holiday and a successful New Year!

Equity and Fixed Income Index returns sourced from Bloomberg on 12/20/24. All FOMC data is sourced from the Federal Reserve Bank. Economic Calendar Data from Econoday as of 12/20/24. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.