Strong Jobs Data Creates Pain for Markets

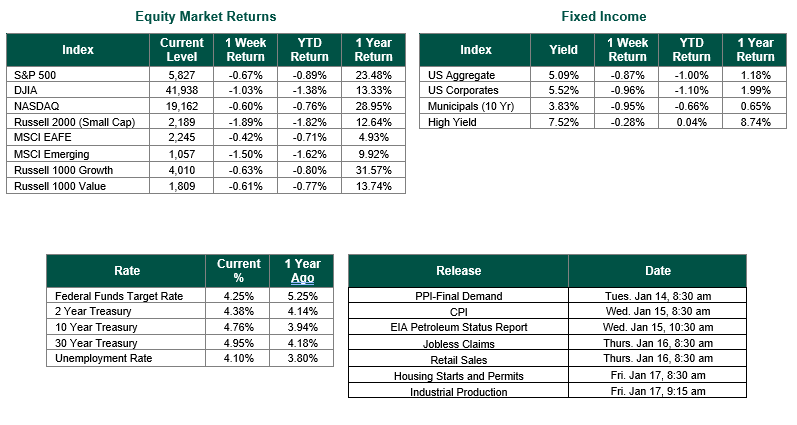

Global equity markets finished higher for the week. In the U.S., the S&P 500 Index closed the week at a level of 5827, representing a decrease of 0.67%, while the Russell Midcap Index fell over 2% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, decreased 1.89% over the week. As developed international equity performance and emerging markets were both negative, returning -0.42% and -1.50%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 4.77%.

The first jobs reports of 2025 for the U.S. painted an encouraging picture. Nonfarm payrolls for December surged to 256,000, significantly exceeding expectations of 165,000. This robust job growth pushed the unemployment rate down to 4.1%, further tightening the labor market. While average hourly wage growth came in slightly below forecasts at 3.9%, this still points to a potential moderation in services inflation, which is a key focus for investors.

These strong employment numbers signal a few important things for the stock market. Firstly, a low unemployment rate generally boosts consumer confidence and spending, which are vital drivers of economic growth. Secondly, wage gains exceeding the rate of inflation mean employees are seeing real income growth, further supporting consumer spending. This combination of factors creates a positive environment for businesses and the overall economy, which is ultimately reflected in stock market performance.

The strong jobs report had a significant impact on the bond market. Government bond yields, particularly short-term yields which are closely tied to central bank interest rates, rose sharply. This increase in borrowing costs weighed on stock prices, especially those of highly valued growth companies, such as those heavily concentrated in the technology sector. Conversely, more defensive sectors like utilities and healthcare generally held up better.

This event serves as a reminder that even in a strong economic environment, market reactions can be swift and unpredictable. While political headlines often grab attention, fundamental economic factors ultimately drive market performance.

Equity and Fixed Income Index returns sourced from Bloomberg on 1/10/24. Jobs data from the Bureau of Labor Statistics on 1/9/2024. Economic Calendar Data from Econoday as of 1/13/24. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.