Tame Inflation Data Push Equities Higher.

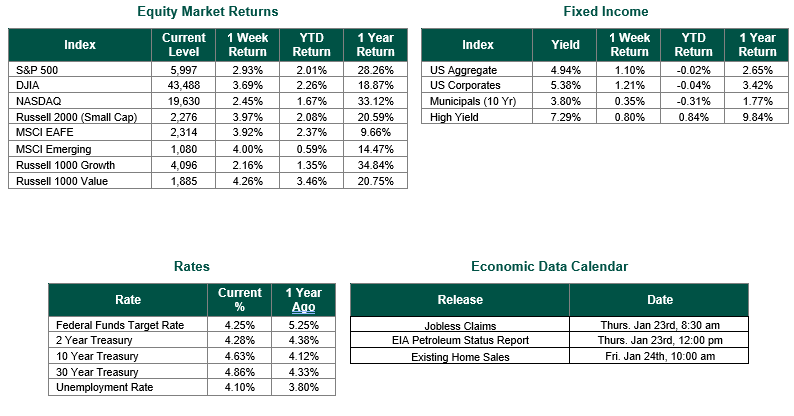

Global equity markets finished higher for the week. In the U.S., the S&P 500 Index closed the week at a level of 5,997, representing an increase of 2.93%, while the Russell Midcap Index moved 4.52% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned 3.97% over the week. As developed international equity performance and emerging markets were both positive, returning 3.92% and 4.00%, respectively. Finally, the 10-year U.S. Treasury yield moved lower, closing the week at 4.63%%.

As our nation prepared for a new Presidential Administration throughout the past week, equity markets moved higher and interest rates moved lower. The movements in the markets were driven by several economic indicators that were released during the week. These economic indicators included the Producer Price Index, the Consumer Price Index and Retail Sales. The markets were looking for directional information concerning inflation and its effect on the Fed’s monetary policy.

On Tuesday the Labor Department reported that U.S. producer prices rose less than expected in December as higher costs for goods were partially offset by stable services prices, suggesting inflation remained on a downward trend after progress had stalled in recent months. The producer price index for final demand rose 0.2% last month after an unrevised 0.4% advance in November, the Labor Department’s Bureau of Labor Statistics said. Economists polled by Reuters had forecast the PPI would climb 0.3%. The narrower measure of PPI, which strips out food, energy and trade, ticked up 0.1% for a second straight month. Core PPI increased 3.3% on a year-on-year basis after advancing 3.5% in November.

The Consumer Price Index released on Wednesday shows that prices that consumers pay for a variety of goods and services rose again in December but closed out 2024 with some mildly better news on inflation, particularly on housing. The index increased a seasonally adjusted 0.4% on the month, putting the 12-month inflation rate at 2.9%, the Bureau of Labor Statistics reported Wednesday. Economists surveyed by Dow Jones had been looking for respective readings of 0.3% and 2.9%. However, excluding food and energy, the core CPI annual rate was 3.2%, a notch down from the month before and slightly better than the 3.3% forecast. The core measure rose 0.2% on a monthly basis, also 0.1 percentage point less than expected.

U.S. retail sales increased in December as households bought motor vehicles and a range of other goods, pointing to strong demand in the economy and further reinforcing the Federal Reserve’s cautious approach to cutting interest rates this year. Retail sales rose 0.4% last month after an upwardly revised 0.8% gain in November, the Commerce Department’s Census Bureau said. Economists polled by Reuters had forecast retail sales, which are mostly goods and are not adjusted for inflation, advancing 0.6% after a previously reported 0.7% rise in November. Retail sales increased 3.9% year-on-year in December.

The report prompted some economists to upgrade their economic growth estimates for the fourth quarter to just shy of the July-September quarter’s brisk pace.

Best wishes for the Week ahead.

Equity and Fixed Income Index returns sourced from Bloomberg on 1/17/25. Producer Price Index and the Consumer Price Index are sourced from the Labor Department. Retail Sales data is sourced from the Commerce Department’s Census Bureau. Economic Calendar Data from Econoday as of 1/17/25. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.