Tariffs Uncertainty Continues as Earnings Season Commences

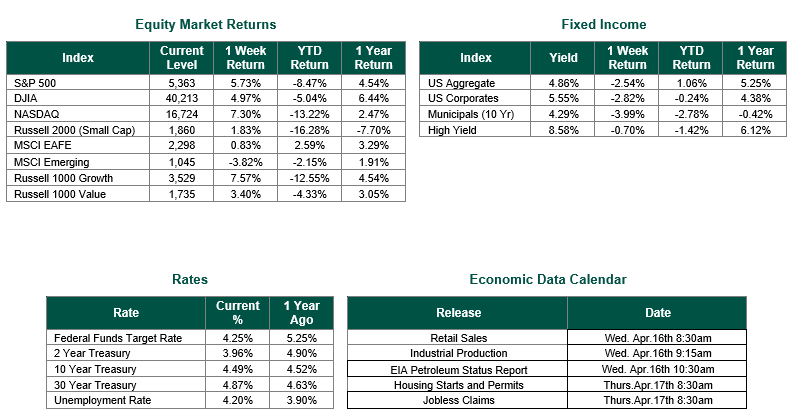

Global equity markets finished higher for the week. In the U.S., the S&P 500 Index closed the week at a level of 5,363, representing a gain of 5.73%, while the Russell Midcap Index moved 6.07% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned 1.83% over the week. As developed international equity performance and emerging markets were mixed, returning 0.83% and -3.82%, respectively. Finally, the 10-year U.S. Treasury yield moved slightly lower, closing the week at 4.49%.

Last week was dominated by ongoing developments concerning international trade tariffs. Global markets fluctuated wildly, with the S&P 500 briefly entering bear market territory on an intraday basis before recovering and closing outside of bear market territory. Not much attention was given to other economic developments during the week. However, we believe that many of these underreported topics are important. They include the Consumer Price Index (CPI), Producer Price Index (PPI), ongoing Capitol Hill discussions concerning the budget and tax policy, and the beginning of corporate earnings season for the first quarter of 2025.

As previously mentioned, trade tensions escalated last week, with significant tariff developments centered around U.S. trade policies. On April 5, a 10% baseline tariff on all imports took effect, as announced earlier on April 2. Higher reciprocal tariffs of 11-50% were scheduled for April 9 but were paused for 90 days for most countries, except China, which faced a 125% tariff rate (stacked on prior levies, totaling 145%). This announcement followed Trump’s threat on April 7 to impose an additional 50% tariff if China did not retract its retaliatory measures by April 8. China increased its tariffs on U.S. goods from 34% to 84% on April 9, then to 125% on April 11, signaling a tit-for-tat retaliation. Beijing also considered export curbs on rare earth minerals but refrained from further non-tariff measures while expressing openness to negotiations.

The CPI showed a decline in consumer prices month-over-month for March 2025, marking the first drop in five years. This reading indicates a temporary easing of inflationary pressures. Initial jobless claims for the week ending March 29, 2025, also decreased to 219,000, down by 6,000 from the previous week. The four-week moving average also saw a slight decline, reflecting a relatively stable labor market. Finally, the PPI for March 2025 rose by 0.2%, following no change in February. This result suggests a modest increase in factory-related inflation, which could impact production costs.

The early releases for first-quarter 2025 corporate earnings have been favorable thus far. Below is a quick recap of key outtakes from some of the more noteworthy earnings reports.

• Delta Air Lines reported better-than-expected first-quarter profit. The airline reported Q1 earnings grew 2% to 46 cents per share while sales increased 3.3% to $12.978 billion.

• JPMorgan Chase reported net income of $14.6 billion and revenues of $45.3 billion, driven by strong performance in investment banking and equity markets.

• Morgan Stanley achieved record net revenues of $17.7 billion, with equity trading contributing $4.1 billion. Net income was $4.3 billion, reflecting a robust quarter.

• BlackRock delivered diluted EPS of $9.64 (or $11.30 adjusted) and saw $84 billion in net inflows, led by iShares ETFs and private markets.

• Bank of New York Mellon managed $53.1 trillion in assets under custody and administration, with $2 trillion in assets under management.

• Wells Fargo reported strong financial results, emphasizing its diversified banking and investment services.

In summary, while international trade tariffs captured headlines and drove market volatility last week, several critical but underreported economic developments also deserve investor attention and consideration. Together, all of these reports paint a multifaceted picture of the current economic landscape that extends beyond trade disputes.

Best wishes for the week ahead, and Happy Easter to all who celebrate!

Equity and Fixed Income Index returns sourced from Bloomberg on 4/11/25. Both CPI and PPI data are sourced from The Bureau of Labor Statistics Economic Calendar Data from Econoday as of 4/11/25. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.

Some of the securities discussed in this update are held in current series of SmartTrust® unit investment trusts (UITs), where Hennion & Walsh serves as sponsor. This update is for information purposes only and should not be used or construed as, an offer to sell, a solicitation of any offer to buy, or a recommendation of the merits of an investment in any security.