Markets React to Military Actions in Iran

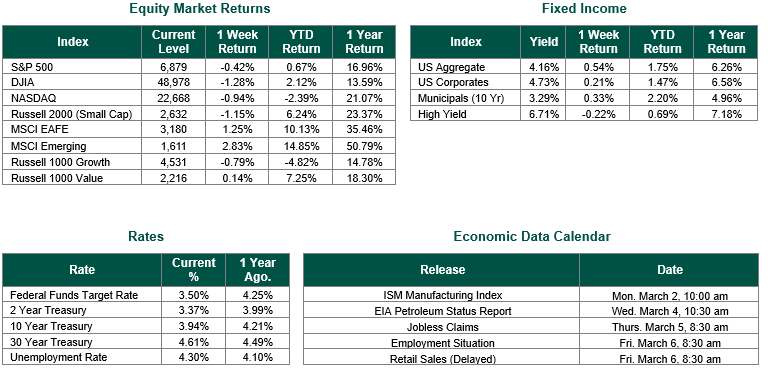

Global equity markets finished mixed for the week. In the U.S., the S&P 500 Index closed the week at a level of 6879, representing a decrease of 0.42%, while the Russell Midcap Index moved +1.66% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -1.15% over the week. As developed international equity performance and emerging markets were positive, returning 1.25% and 2.83%, respectively. Finally, the 10-year U.S. Treasury yield moved lower, closing the week at 3.94%.

As we start the week, we must first acknowledge the joint U.S./Israel operations in Iran that started over this past weekend. Domestic markets are likely to trade with a defensive tone this week as investors digest the widening geopolitical shock from “Operation Epic Fury” and its implications for energy prices, inflation, and economic growth across the globe. Equity futures were pointing lower early on Monday morning, with Dow, S&P 500, and Nasdaq futures all indicate lower levels as investors rotated out of risk assets and into traditional safe havens. Our thoughts and prayers are with the brave men and women of the U.S. military and our allies during this conflict in the Middle East.

In other news, several reports on the U.S. economy were released last week, which painted a picture of cooling but still resilient growth, with softer manufacturing momentum, cautious but improving consumers, a relatively stable labor market, and firm producer-level inflation pressures.

To start, factory orders for December 2025 declined 0.7%, a pullback after a strong 2.7% gain in November, suggesting some late‑year moderation in manufacturing demand even as shipments continued to edge higher, up 0.5% in December and extending earlier gains.

Consumer confidence for February moved up to 91.2 from a revised 89.0 in January, indicating a modest improvement in sentiment, though the level remains well below the highs seen in 2024 and consistent with a still cautious outlook on the economic environment.

Labor market data released last Thursday showed initial jobless claims rising slightly to 212,000 for the week ending February 21, up 4,000 from the prior week but still near historically low levels, reinforcing the view that layoffs remain limited and that the job market is stabilizing rather than weakening materially.

On Friday, the January Producer Price Index (PPI) report showed final demand prices up 0.5% on the month and 2.9% year over year, with much of the gain driven by services and core components, signaling that upstream inflation pressures remain present even as overall price increases have moderated.

Taken together, all of last week’s releases suggest an economy transitioning into a slower but still expanding phase: manufacturing is cooling at the margin, households are slightly more optimistic but far from exuberant, employers are holding onto workers, and inflation at the producer level is running at a pace that keeps monetary policy considerations front and center, and additional near-term interest rate cuts unlikely.

Equity and Fixed Income Index returns sourced from Bloomberg on 2/27/26. Factory Orders were sourced from the U.S. Census Bureau. The Consumer Confidence Index was sourced from The Conference Board. Weekly Jobless Claims are sourced from the U.S. Department of Labor. Producer Price Index (CPI) was sourced from the Bureau of Labor Statistics. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.