Corporate Earnings are Booming!

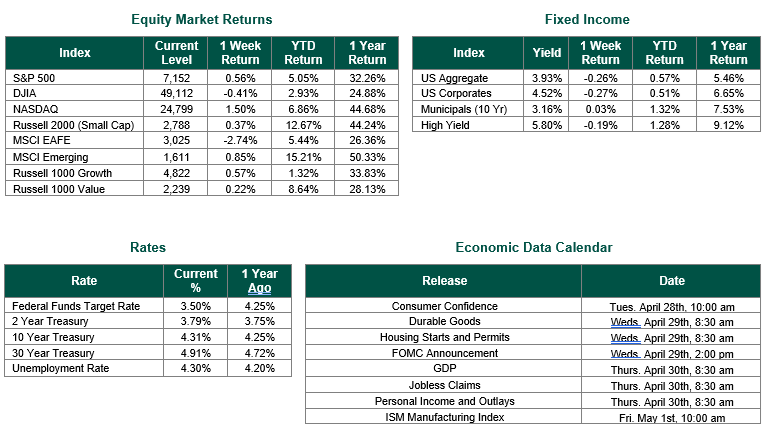

Global equity markets finished mixed for the week. In the U.S., the S&P 500 Index closed the week at a level of 7,152, representing an increase of 0.56%, while the Russell Midcap Index moved -0.38% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned 0.37% over the week. As developed international equity performance and emerging markets were mixed, returning -2.74% and 0.85%, respectively. Finally, the 10-year U.S. Treasury yield moved higher, closing the week at 4.31%.

Our update this week focuses on underlying economic fundamentals rather than geopolitical risk, which the conflict with Iran has certainly elevated. The emphasis is on what the latest earnings and macroeconomic data reveal about growth, profitability, consumer demand, and labor-market conditions, rather than on the market impact of conflict-driven headlines and uncertainty.

Using FactSet data, the S&P 500’s Q1 2026 earnings season got off to a strong start, with 28% of index companies having reported and results running ahead of typical historical patterns. FactSet said 84% of those companies beat earnings per share (EPS) estimates, the average EPS surprise was 12.3% above estimates, and the blended S&P 500 earnings growth rate stood at 15.1%, alongside revenue growth of 10.3%.

The tone across reported companies was broadly positive. FactSet highlighted especially strong contributions from Industrials, Information Technology, Health Care, Materials, and Financials, while Energy and Health Care were the main sectors restraining year-over-year earnings growth thus far. Among the most notable company-level EPS beats were GE Vernova, Intel, Micron Technology, Netflix, and several large financials, with GE Vernova’s results notably boosted by a large M&A gain.

Revenue results were also holding up well, with 81% of reporting S&P 500 companies beating revenue estimates and aggregate revenue coming in 2.0% above expectations. FactSet noted that all 11 sectors posted year-over-year revenue growth, led by Information Technology, Communication Services, and Financials, suggesting the season is being driven predominantly by genuine top-line expansion rather than cost-cutting alone.

Profitability was strong as well. FactSet reported a blended net profit margin of 13.4% for Q1 2026, above the prior quarter and the year-ago period, and, if finalized, the highest margin the firm has tracked since 2009. That combination of above-average EPS beats, solid revenue growth, and record-high margins points to an earnings season that has been stronger than analysts expected heading into the quarter. The question now becomes how much longer earnings, revenues, and profits can remain this strong.

On the economic data front, last week brought a mixed but still resilient set of U.S. readings. Retail sales for March were expected to show that consumer spending remained solid, with the prior report described as modestly higher and consistent with a consumer who was still spending but becoming more selective. Weekly jobless claims remained an important gauge of labor-market cooling, after initial claims rose to about 219,000 and continuing claims eased to around 1.79 million, suggesting layoffs had edged higher, but job finding remained relatively stable.

The April flash PMIs were the key growth indicators of the week, following March data that showed a split economy: manufacturing stayed in expansion at 52.3, while services slipped into contraction at 49.8, the first sub-50 reading in more than two years. That made the April composite PMI an especially important signal for whether broader business activity was stabilizing or still losing momentum. Friday’s final University of Michigan consumer sentiment reading was expected to confirm very weak household confidence after the preliminary April figure fell sharply to 47.6, while one-year inflation expectations rose to 4.8% and long-run expectations increased to 3.4%. Taken together, the data pointed to an economy that remained resilient across several hard-data categories, but consumer confidence and parts of the services sector showed clear strain.

Our thoughts remain focused on the brave Men and Women of the U.S. Military and our Allies during the ongoing conflict in the Middle East.

Equity and Fixed Income Index returns sourced from Bloomberg on 4/24/26. Corporate earnings data are sourced from FactSet. Retail sales data is sourced from the U.S. Census Bureau. Weekly Jobless Claims are sourced from the U.S. Department of Labor. PMI data is sourced from S&P Global. Consumer Sentiment data are sourced from the University of Michigan. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio, but it does not ensure a profit or guarantee against a loss.