Dow Sets Off Fireworks with Record High

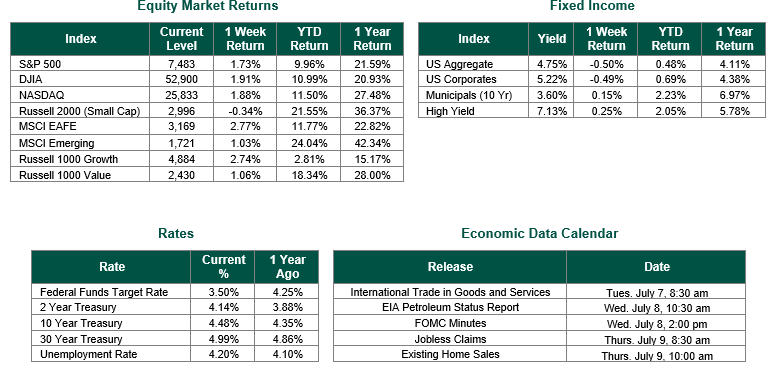

Global equity markets finished mixed for the week. In the U.S., the S&P 500 Index closed the week at a level of 7483, representing an increase of 1.73%, while the Russell Midcap Index moved +0.35% last week. Meanwhile, the Russell 2000 Index, a measure of the Nation’s smallest publicly traded firms, returned -0.34% over the week. As developed international equity performance and emerging markets were positive, returning +2.77% and +1.03%, respectively. Finally, the 10-year U.S. Treasury yield closed the week at 4.48%.

Last week was defined by a broadening rally across traditional market sectors, renewed weakness in semiconductors, and a softer-than-expected June jobs report that eased fears of a potential Federal Reserve interest rate hike. In a holiday-shortened week that saw U.S. markets closed Friday for the Independence Day holiday (Happy 250th birthday, America!), the Dow Jones Industrial Average notched a fresh all-time high on Thursday. However, the technology-laden Nasdaq composite index lagged as a global chip selloff, sparked in part by a sharp decline in South Korean semiconductor names, dented what had been the market’s most reliable leadership group. Beneath the surface, the rotation story was the most encouraging development of the week, with market breadth broadening meaningfully and leadership expanding into banks, industrials, commodities, utilities, and dividend-paying names that have spent much of 2026 in the shadow of the AI trade – though some of them, notably industrials and utilities, are benefactors of the AI revolution.

The June nonfarm payrolls report, released last Thursday morning ahead of the holiday, was the most consequential economic event of the week. The economy added just 57,000 jobs in June, well below the 113,000 consensus estimate and a meaningful step-down from the recent trend. Compounding the softness, prior-month revisions subtracted an additional 74,000 jobs from April and May combined. The unemployment rate ticked down to 4.2% from 4.3%, though this decline was driven largely by a 720,000 drop in the labor force rather than by stronger hiring, with labor force participation falling to 61.5%. Wage growth held steady at 3.5% year-over-year, in line with expectations and consistent with contained services inflation. Taken together, the report broke a three-month streak of hotter-than-expected labor data and supported the case for the Fed to keep rates steady in the near term, easing recent concerns about a potential rate hike.

The reaction to the jobs report also underscored a subtle but important shift in how markets are digesting communications from the Federal Reserve under new Chairman Kevin Warsh. In a notable break from his predecessor Jerome Powell, Warsh has explicitly urged Wall Street to look to the incoming data, rather than to the Fed itself, to map out the likely path for interest rates. This deliberate step back from forward-looking guidance marks a meaningful stylistic and philosophical departure and effectively places greater weight on each economic release. In the current environment, with the June FOMC dot plot revealing a deeply divided committee with roughly half of members favoring a rate hike by year-end and the other half favoring holding steady or cutting. The market’s dependence on the data has arguably never been greater. Investors should expect heightened sensitivity to each incoming inflation, employment, and growth release in the months ahead.

Looking to the week ahead, the release of the minutes from the June FOMC meeting on Wednesday will be the primary focus for investors, offering a deeper look into the committee’s split views on the path of policy and any additional color on Chairman Warsh’s approach. With the Fed increasingly emphasizing data dependence, incoming inflation reports over the coming weeks will carry heightened importance, particularly the June Consumer Price Index (CPI) release later this month. Second-quarter earnings season is also just around the corner, with the major banks kicking off reporting the following week, and expectations calling for another solid quarter of profit growth despite the more uneven macroeconomic backdrop. Ongoing developments around the U.S.-Iran framework agreement, oil prices, and global trade negotiations will also remain in focus.

Best wishes to all for the week ahead!

Equity and Fixed Income Index returns sourced from Bloomberg on 7/2/26. Unemployment data sourced from the Bureau of Labor Statistics on 7/2/26. Weekly Jobless Claims are sourced from the U.S. Department of Labor. International developed markets are measured by the MSCI EAFE Index, emerging markets are measured by the MSCI EM Index, and U.S. Large Caps are defined by the S&P 500 Index. Sector performance is measured using the GICS methodology.

Disclosures: Past performance does not guarantee future results. We have taken this information from sources that we believe to be reliable and accurate. Hennion and Walsh cannot guarantee the accuracy of said information and cannot be held liable. You cannot invest directly in an index. Diversification can help mitigate the risk and volatility in your portfolio but does not ensure a profit or guarantee against a loss.